1 min read

7 min read

![7 Most Common Money Mule Red Flags in 2026 [Explained]](https://www.acoru.com/hubfs/Cover-1.webp)

Money mule red flags are indicators that a customer may be using their account to move money linked to financial scams or other fraudulent activity.

Because mule activity often resembles legitimate transactions, these schemes can be difficult to detect before losses occur. According to the US Federal Reserve's 2026 Risk Officer Report, 49% of banks only identified mule accounts after suffering losses.

In this article, we will explore seven of the most common money mule red flags and how you can spot them early to strengthen your fraud and AML controls.

Key Takeaways

- Money mule activity often hides in normal-looking accounts

Criminals frequently recruit students, young adults, and financially vulnerable individuals through fake jobs, romance scams, and social media. Many mules are unaware they are helping launder illicit funds, making detection more challenging.

- Subtle changes in context and trajectory are stronger indicators than individual transactions

Sudden spikes in account activity, unexpected deposits from unrelated parties, and rapid movement of funds are some of the clearest warning signs. Looking at how account context changes over time is often more effective than focusing on transactions alone.

- Connected signals reveal risks that isolated controls miss

Suspicious device activity, unusual IP locations, reluctance to complete KYC checks, and networks of linked accounts often point to coordinated mule operations.

- Banks need proactive monitoring

Behavioral analytics, transaction monitoring, network analysis, enhanced due diligence, and continuous account intelligence help identify suspicious activity earlier and reduce financial and compliance risks.

- AI-native account intelligence can improve early detection

Acoru helps financial institutions detect risks earlier by continuously evaluating risk across channels and data sources to classify accounts and their counterparties. It works as a holistic solution but can also enhance existing fraud and AML systems (no rip and replace) to uncover mule networks, prevent losses, and support evolving regulatory requirements.

What Is a Money Mule?

A money mule is someone who transfers, moves, or converts money obtained through criminal activity on behalf of another person. Criminals use money mules to distance themselves from money made through illegal activities, making it harder for law enforcement to trace where the funds came from.

Depending on their level of awareness and involvement, money mules generally fall into three categories:

- Unknowing (unwitting) individuals: These people are unaware that they are involved in a money-laundering scheme.

- Witting individuals: They generally recognize that something is unusual or suspicious but choose to ignore the warning signs or avoid asking questions. They typically receive financial compensation for their involvement.

- Complicit individuals: These are professional money mules who knowingly participate in laundering criminal proceeds. They are often experienced and familiar with methods used to reduce the risk of detection.

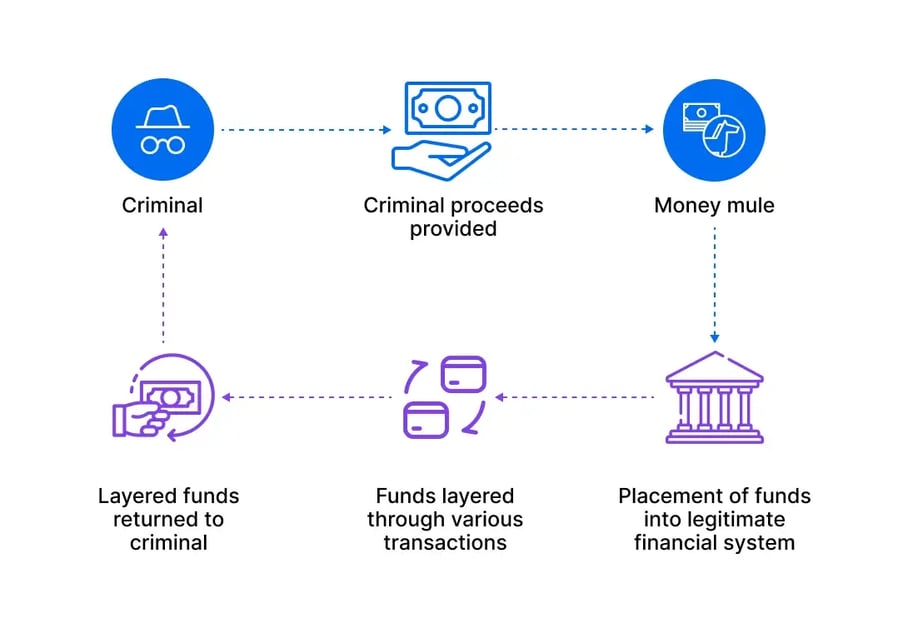

How Money Mules Are Used in Fraud

The process of money muling typically involves four stages:

Stage 1: Recruitment and Onboarding

Criminals target potential money mules through social media, online job ads, dating apps, or even personal connections. They often promise easy money for minimal effort and persuade victims to share personal information, banking details, or account access.

Stage 2: Account Setup

Recruits may be asked to use their existing bank accounts or open new ones. In some cases, criminals might instruct them to create digital wallets or provide access to services such as remote deposit capture.

Stage 3: Moving and Disguising the Funds

Funds obtained through fraud, scams, and other financial crimes are deposited into the mule's account through cash deposits, wire transfers, ACH credits, or peer-to-peer payment services.

The mule is then instructed to move the money quickly, often through multiple accounts, cash withdrawals, or conversion into digital assets.

These transactions are often completed within hours, making them significantly more difficult for financial institutions and law enforcement to trace.

Stage 4: Payout and Commission

The mule typically keeps a small percentage of the money as payment and forwards the remainder to the account provided by the criminals.

7 Most Common Money Mule Red Flags You Should Know

No single indicator is enough to prove wrongdoing, but certain patterns can raise concerns. Below are seven money mule red flags that may signal potential misconduct:

1. Unusual Account Holder Demographics and Occupations

While money mules can come from any demographic, criminals frequently target younger individuals, students, and financially vulnerable people through social media and online job offers.

In the UK, the Financial Conduct Authority reported that 207,889 personal accounts were used for money muling in 2024, with one-third of those involved aged 22–29 and nearly one-fifth under 21.

2. Unexpected Deposits from Unknown Sources

Large or multiple incoming transfers from individuals or businesses with no apparent relationship to the account holder can signal that the account is being used to move money on behalf of others.

Worth knowing:

Acoru continuously evaluates both customer and counterparty accounts to build an ongoing risk profile for all accounts your customers interact with. This helps financial institutions identify potentially risky counterparties and detect suspicious payment relationships earlier, even in external financial institutions, rather than relying on individual transactions or sessions alone.

3. Sudden Changes in Account Activity

A significant shift in an account's normal transaction patterns can indicate money mule activity. Previously inactive or low-volume accounts that suddenly begin receiving numerous payments or handling amounts that are inconsistent with the customer's profile or historical behavior warrant closer review.

For example, a student account that previously processed a few hundred euros per month may suddenly process €20,000 in small, incoming transfers from 20 or 30 unrelated individuals.

Worth knowing:

Solutions like Acoru help uncover high-risk activity before it escalates. By continuously updating account risk as new signals emerge across channels and data sources, Acoru identifies gradual behavioral changes that may indicate an account is transitioning to money-mule activity.

4. Rapid In-and-Out Transactions

Money mules are often instructed to move funds quickly to avoid detection. A common pattern involves multiple small deposits followed by immediate transfers, withdrawals, or payments, leaving little or no money in the account.

This activity is particularly suspicious when it occurs shortly after the account is opened, especially when the same pattern appears across several newly created accounts.

5. Transfers to High-Risk Jurisdictions and Risky Counterparties

Frequent international transfers to multiple accounts, particularly in countries identified as high-risk by the Financial Action Task Force (FATF), such as Iran, North Korea, and Myanmar, or in jurisdictions under increased monitoring, are a common warning sign of mule activity.

Transfers to countries with weak anti-money laundering (AML) controls should also be viewed as higher-risk activity and examined more closely.

6. Suspicious Device or IP Activity

Money mule activity often shows up through unusual account access patterns. For example, accounts being accessed from multiple IP addresses, through VPNs or anonymizing services, or from different locations within a short period of time can suggest that someone other than the account owner has access to the account.

Another red flag is when several customer accounts are accessed from the same device, which may point to coordinated activity.

7. Reluctance to Provide KYC/AML Information

Money mule accounts are often associated with customers who are unwilling or unable to complete standard identity verification procedures. Common warning signs include:

- Delays in providing identification documents

- Inconsistent or contradictory personal information

- Failed customer due diligence (CDD) checks

- Repeated attempts to avoid or bypass verification requirements

How Banks Can Respond to Common Money Mule Red Flags

The table below outlines practical actions you can take to investigate and mitigate each of these money mule red flags:

|

Red Flag |

What Banks Can Do |

|

1. Unusual account demographics and occupations |

• Apply risk-based monitoring to vulnerable customer segments • Compare account activity against declared occupation, income, and expected account usage • Perform periodic customer reviews when transaction volumes are inconsistent with the customer profile • Increase awareness efforts and educate customers about money mule recruitment tactics |

|

2. Unexpected deposits from unknown sources |

• Generate alerts for multiple incoming payments from unrelated counterparties • Review transaction details and counterparty relationships • Contact the customer to establish the source and purpose of funds |

|

3. Sudden changes in account activity |

• Use behavioral analytics to identify abnormal changes • Compare transaction activity against historical patterns and expected account usage • Request additional information regarding the nature of transactions |

|

4. Rapid in-and-out transactions |

• Monitor for pass-through transactions and short holding periods • Detect structuring patterns intended to avoid reporting thresholds • Apply transaction limits or temporary holds while reviewing activity |

|

5. Transfers to high-risk jurisdictions and risky counterparties |

• Screen counterparties and countries against FATF and sanctions lists • Apply enhanced due diligence to higher-risk international transactions • Review repeated transfers to the same beneficiaries • Investigate unusual IP locations and transaction origins |

|

6. Suspicious device or IP activity |

• Monitor device fingerprints and IP addresses • Detect impossible travel scenarios and anonymizing services • Identify shared devices across multiple customer accounts |

|

7. Reluctance to provide KYC/AML information |

• Pause onboarding or restrict account functionality until verification is completed • Validate identity documents and screen customer information • Decline account opening or terminate relationships where necessary |

Detect Money Mule Activity with Acoru Before Payment Is Initiated

Money mule activity rarely presents itself through a single indicator. Warning signs often appear across different channels, accounts, devices, and time periods.

As criminals increasingly rely on account networks and sophisticated scams, many institutions are complementing their existing fraud and AML controls with continuous account intelligence.

By orchestrating signals from multiple channels and data sources into a single account view, institutions can continuously assess account risk, strengthen money-mule detection, and support compliance with evolving regulatory requirements. This is where Acoru can help.

Acoru is an AI-native fraud platform that provides continuous account intelligence to help financial institutions detect mule activity and scam-related risks before transactions are initiated.

Rather than focusing solely on transactions, Acoru evaluates risk signals across channels and data sources to classify accounts and their counterparties and maintain an up-to-date view of account risk.

The platform complements existing fraud and AML systems without requiring institutions to replace their current technology stack. It also supports compliance with regulatory frameworks such as PS23/4, PSD3, and other emerging fraud and AML requirements.

Acoru's Key Capabilities

Here is how Acoru can help you strengthen your institution's money mule detection:

- Continuous account classification – Acoru continuously evaluates account risk and classification, distinguishing between regular accounts, victims, mule accounts (including unwitting, witting, and complicit classifications), money laundering accounts, and honeypots.

- Mule network and counterparty intelligence – Acoru evaluates relationships between accounts and counterparties, analyzing risk signals from channels and other data sources to uncover coordinated mule activity and provide you with risk context for both internal and external accounts.

- Pre-fraud signal detection – Acoru monitors risk signals that often appear before a transaction is initiated, including new payees, test payments, profile changes, unusual login behavior, channel switching, and counterparty anomalies.

- Omnichannel intelligence – Acoru brings together data from multiple channels, sources, and systems to create a single account-centric view of risk, helping you detect patterns that siloed solutions may miss.

- Consortium intelligence – Through privacy-preserving collaboration, Acoru gives you access to ecosystem-wide intelligence, helping you identify mule networks and high-risk destinations that may not be visible within your own institution's data.

Request a demo today and discover how continuous account intelligence can help you uncover mule networks.

FAQ

1. Which accounts are most vulnerable to money mule abuse?

Accounts belonging to students, young adults, newly onboarded customers, and financially vulnerable individuals are often targeted by criminals. However, any account can be exploited if fraudsters gain access or recruit the account holder.

2. How often should banks review customer risk profiles for potential mule activity?

Customer risk profiles should be reviewed continuously or whenever significant behavioral changes occur. Periodic reviews combined with continuous monitoring can help you detect emerging risks earlier.

1 min read

Uncovering Money Mule Networks

Real-time payments have redefined how we move money; it’s now fast, frictionless, and always on. For people and businesses, modern money transfer...

1 min read

The Different Roles of Money Mules in Fraud Operations

Money mule activity is often treated as a single category of risk. An account is flagged as a “mule,” controls are applied, and the case moves...